George Soros and Bank of America Merrill Lynch appear to have a significant difference of opinion regarding Greece.

One analyst, a hedge fund legend best known for “bringing down” the Bank of England, looks at the dispute from the perspective of the Greek people and knows that compounding debt and government-imposed hardship likely will not last. The other looks at the situation from a financial engineering standpoint, safe and secure in the knowledge that such economic hardships will not likely touch their relatively individually charmed economic life. One analyst is likely the more realistic.

Soros: “Greece still a problem”

In a speech yesterday at the World Economic Forum, hedge fund manager George Soros voiced a consistent opinion. The man known for his power over central bankers – a rare achievement for a hedge fund manager – told Bloomberg’s Francine Lacqua that “Greece is still a problem,” one that “has no solution, because it has been so messed up.”

Considering historical context to a degree, Soros bases his logic, to a degree, on how much pain common people can endure. Contrast this with a January 21 Bank of America Merrill Lynch report notes as a positive that “ambitious pension reform and new taxes for farmers” is part of a market positive, the extent to which the Greek people will be willing to suffer without revolt remains to be seen.

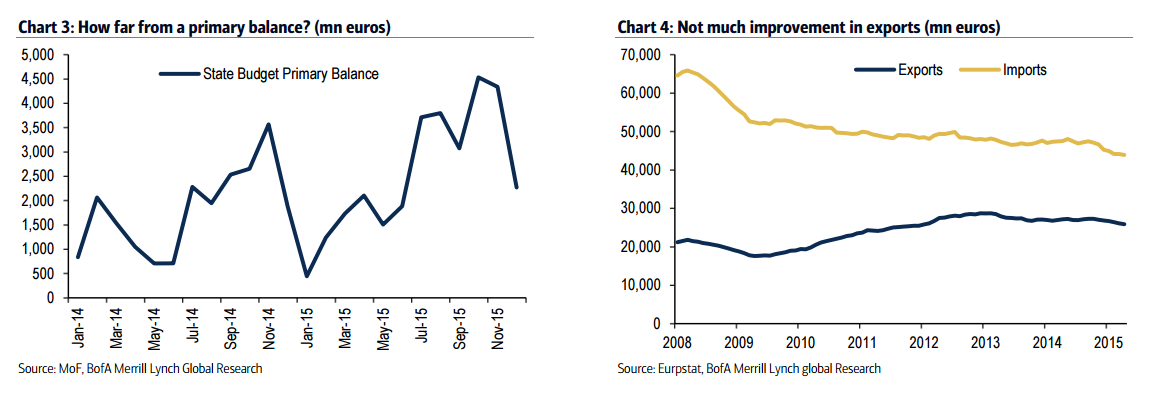

BAML: Greece has moved to a much better place

The generally optimistic bank report, titled “Greece – one EM with a positive trigger,” speaks from the European banking establishment script. “Greece has moved to a much better place since coming very close to Grexit last July,” the BAML report said. “Although we don’t expect substantial debt relief—only some maturity extension, gradual and subject to strict conditions—we believe any such action would still send a positive market signal.”

The BAML report makes it clear: There will be no debt reduction for Greece as was given to Germany after World War II in theLondon Accord. There will only be maturity extensions, which means additional compounding debt mounting to the point the country literally cannot bleed anymore. At this point Greece either revolts from the system or the sovereign nation and its assets become a wholly owned subsidiary of bond investors.

This perhaps highlights one of the most obvious distinctions between debt analysts from major banks, who at times oddly all take up the same talking points. Consider, for instance, the case of Petrobras 100 year bonds, a topic we highlighted in ValueWalk. While hedge fund leader Bridgewater Associates provided the most accurate analysis, saying the bonds were a risky investment in part due to rather obvious compounding concerns including overwhelming debt, fraud and a lack of proper analysis, the bank’s opinion differed dramatically.

This resulted in a back and forth argument, but the issue was ultimately settled. The result? Petrobras and the banks who marketed the debt are now subject of a $98 billion lawsuit. Institutional investors such as the Bill and Melinda Gates Foundation will have less capital for their good works as a result of the alleged misconduct in the bond offering.

Bank report says Greece can long for QE stimulation to caress the nation’s elite as reason to stand united in the Eurozone

Debt is a compounding problem that the banks have a consistent record at underestimating. Soros thinks there is “no solution” to Greece and the “problem is now coming to the boiling point again.”

Bank of America Merrill Lynch sees it differently. While the report does outline risks in relatively muted terms, it considers success from a financial engineering standpoint which doesn’t address the central issue. If the Greeks mind their manners by “mid-2016,” the report observes that the country could be allowed to “participate in the ECB’s QE by the fall, as Draghi promised during the October ECB meeting.” Joy of all joys for those trading in high end assets in the country. “After Greece joins QE (assuming it is able to participate), Grexit risks would be reduced substantially.” Lowered borrowing costs could increase recovery prospects, the bank report said, as if talking directly from the central banker script. This could result in Greece linking its future with quantitative financial engineering and they “may even be able to re-access market before the end of the year.”

{kind=link}