Greece has returned successfully to capital markets

Spreads between Greek and German bonds widening

Greece will remain dependent on financial support

The Eurozone member where the sovereign debt crisis began, Greece, is still far from completing a full economic recovery. Of course, when circumstances are dire, one takes what good news one can, e.g. the government budget points to a primary surplus of EUR 812 million this year. Similarly, in the current low bond yield environment, Greece was able to lure investors as it made a successful return to the international capital markets in April.

Greece is so fragile, just one minor event could throw it back into chaos. Photo: Thinkstock

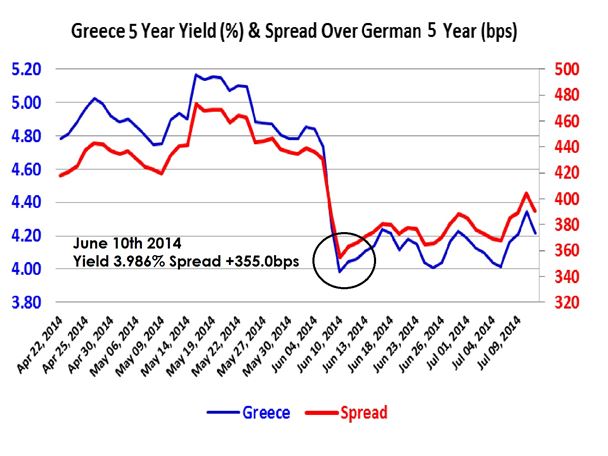

The national treasury placed EUR 3 billion of 5-year bonds at an interest rate of 4.95 per cent. The yield did fall in the secondary market to 3.986 percent on June 10th when the spread over German 5-year BOBL’s contracted to +355 basis points. However, since then the yield and spread have started to widen, see chart, with excellent rotation in the channel to close last week at a yield of 4.214 per cent and a spread of +390.6 basis points .

Source: www.investing.com, Spotlight Ideas

I find it incredible that Greece was allowed to openly raise more debt when the politicians had delayed until the 11th hour a program of reforms that had already been agreed with the Troika. This last ditch implementation was undertaken solely so as to receive the disbursement of the next tranche of bailout funds.

Greece had to find EUR9.3Bn cash to redeem debt maturing in May. Bailout money in May and the new bond issue has simply been used to pay old debts. Maybe it is just me, but it’s hard to see much progress there.

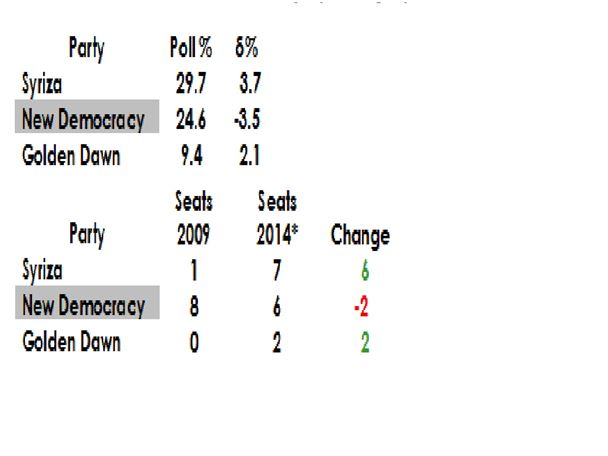

However, dealing with the reality/fantasy that is Eurozone finance, there was never really a doubt that the Eurogroup decision last week would be to approve the latest tranche of aid for Greece. Still, even with access to the capital market and with the previously agreed rescue funds now expired, Greece is likely to remain dependent on financial support from its international lenders. I remain convinced that Greece teeters on the edge of a political crisis. We see in the opinion polls the centre-left group, PASKOK has vanished and key gains since the last general election have all been made by Syriza and Golden Dawn. The Greek results at the recent European Parliamentary Elections showed Syriza with a lead of over 5 percent on New Democracy.

Source: Greek Election Commission, European Parliament New Democracy Party in power

The leader of Syriza, Alexis Tsipras will not act over the long summer but he could consider forcing an early general election this autumn, which is currently scheduled for June 16, 2016. He would point to the fact that Greece has suffered an economic depression since 2008 and on October 14 2013 the Europen Central bank said that Greece would need a third bailout on top of the EUR 240 billion that has already been extended to the nation.

It stated that the nation has had to endure several rounds of internal devaluation that has taken a toll. Public sector budgets have been slashed in terms of headcount and the average level of take home pay for those that still held a job. However, successive governments have failed to make significant inroads into the high level of tax evasion.

Source: Eurostat

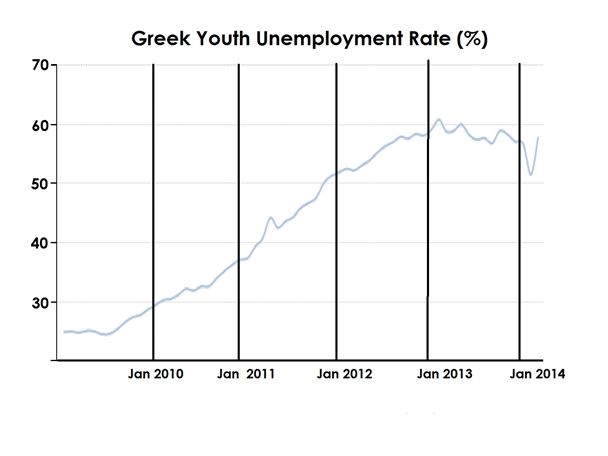

Greece faces significant social difficulties as a result of the austerity it has endured since 2009. Unemployment is set to remain elevated amid public-sector cuts and structural reforms that make hiring and firing easier. In particular, youth unemployment (see above) has reached crisis proportions and risks producing a "lost generation" of individuals with little work experience and hence rapidly diminishing employability, leading to negative impacts both for their personal prospects and for their countries' long-term growth.

There is growing resentment within the population of ordinary Greeks who are commanded to make payments at local tax offices while the largest tax offenders appear to get away with non-payment. The official line from the central government is that it is too complicated to tackle their sophisticated tax sheltering systems.

ECB President Mario Draghi has cautioned that reform fatigue has recently set in among the government even though Eurogroup said the Greeks have committed to completing the second set of milestone reforms by early August.

After the bond issue in April the Prime Minister Antonis Samaras said “Greece is back”. That is far too complacent a remark to make. Just look at the longer part of the curve; on the week the Greek 10-year yield rose from 5.94 percent to 6.34 percent and the spread over Germany widened from 468 basis points +513 basis points.

Mr Samaras should be more careful in choosing his words for we all know what follows pride. Greece is so fragile it would take just one minor event, that could be perceived as systemic, to throw Greece off its grudging recovery track and back into chaos. If that happens, the undertow could yet create trouble in the broader Eurozone.

{kind=link}